2022 Mid-Year Update: The Long and Winding Road

2022 Mid-Year Update: The Long and Winding Road

June 20th, 2022

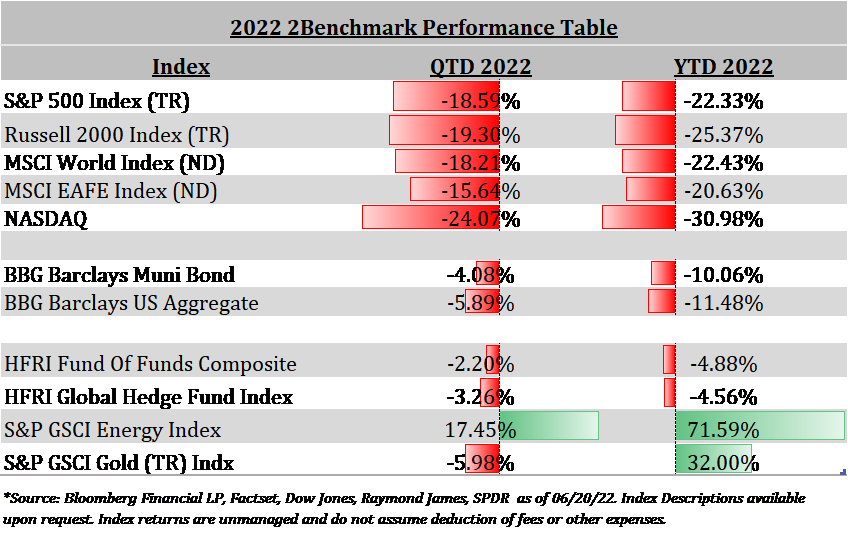

The first 6+ months of 2022 have been among the most difficult macro environments that investors have faced in the last decade. Soaring inflation, exacerbated by the Ukraine situation, and growing fears of recession have led virtually all risk assets lower. Compounding the pain, we are experiencing an unusually high correlation between equity and fixed income returns. Bonds in general have not been a refuge for investors as yields have ticked up sharply in response to extreme inflation readings and the Fed’s announced and anticipated interest rate increases. Crypto bulls have learned a painful lesson that Bitcoin and its counterparts are not, in fact, a safe haven asset. Virtually the only positive performance we have seen year to date in the public markets has come from commodities, with energy prices in particular ripping to the upside in response to Russian supplies evaporating from much of the world market.

Inflation: Not So Transitory

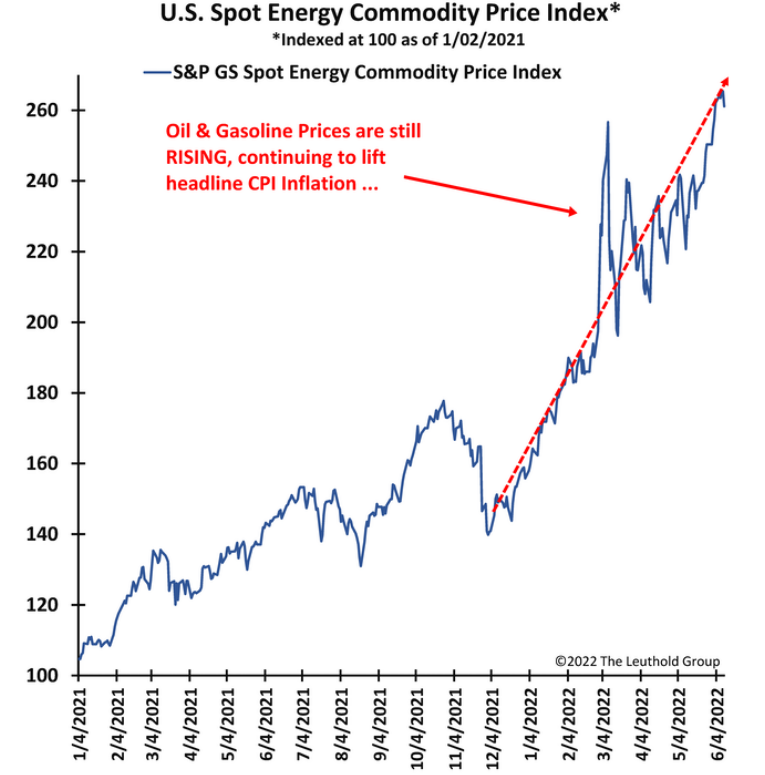

Elevated inflation readings have been present for well over a year, with Fed Chairman Powell and economists only recently abandoning the transitory label. Massive injections of liquidity following the COVID-19 induced economic shut down and resulting supply chain disruptions initially spawned persistent increases in food, energy, and many durable goods. Housing prices soared as low interest rates spurred new home purchases and housing starts while rents simultaneously increased. The Fed remained extremely accommodative well into 2022, adding fuel to the burning coals. Vladimir Putin’s imperialist invasion of Ukraine quickly sent oil prices soaring as Russian supplies were almost immediately sanctioned by many of the world’s largest economies. Additionally, we have experienced extremely low capital investment in the energy complex and are currently at decade low rig counts as policymakers have continued to push more clean energy initiatives, resulting in a lower amount of institutional capital in the space. China’s zero tolerance Covid policies and corresponding economic shutdowns have further hampered supply chains. Throw it all together and voila, we get the recent 8.6% annualized inflation reading and gas prices over $5 per gallon. Not a macro environment that risk assets respond positively to.

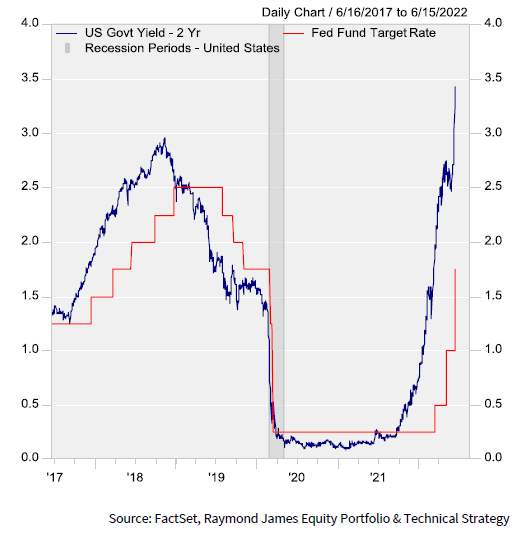

Last week’s higher than expected CPI reading spurred the Fed to pivot quickly and raise the Fed Funds rate by .75% (more than the originally anticipated .50%). Currently, the market expectation is for another .75% increase in July, pushing the upper end of the Fed target rate to 2.5%. Now the Fed faces a challenging task; be hawkish enough to temper inflation but agile enough to not over tighten. Historically, the 2-year Treasury yield has been a particularly good indicator of where the Fed is headed. Currently at 3.19%, the Fed is quickly playing catch up to where the bond market believes the Fed needs to go with rates.

Meanwhile, some macro data seems to indicate that the US economy is softening. Consumer confidence moved to a new low, while retail sales ex-auto missed expectations. Higher interest rates seem to have already impacted housing via higher mortgage rates, as home starts had a huge miss vs. consensus expectations. Manufacturing also seems to be slowing, with both Empire Manufacturing indexes missing expectations to the downside.

High energy prices have been the biggest contributor to the spike in headline inflation, with US energy prices currently more than 2.5 times higher than the start of 2021. Much of the gains have taken place since the onset of the Russia / Ukraine conflict, and we are unlikely to see much if any relief until some sort of resolution is reached on the matter. In the meantime, if energy price increases can level out or moderate, we should see relief on the headline inflation numbers.

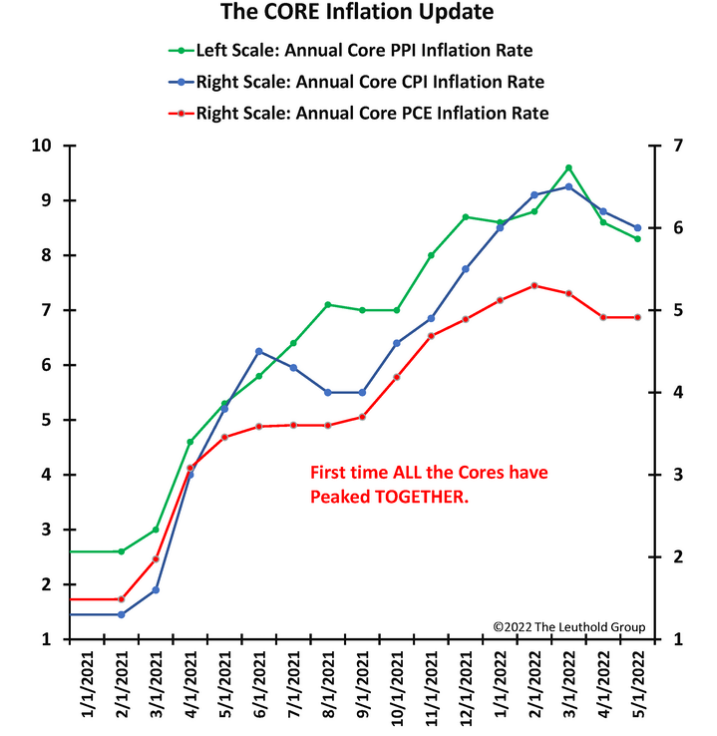

Not all the news appears to be bad. We have seen prices in other commodities, including agricultural, soften and industrial commodities weaken. Additionally, while the headline CPI numbers have soared, core inflation numbers have moderated in the last two months.

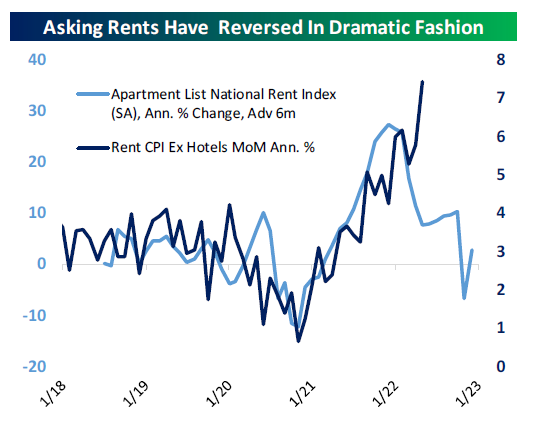

Additionally, 41% of the advance in core CPI over the last three months came from pandemic-related categories, with airline fares having the biggest impact. Rents have also been significant problem, with rent ex-hotels accounting for 42% of the advance. But rental tightness has likely passed, with median asking rents plunging and likely lower realized rents going forward. Other encouraging signs include used car prices rising slower in May and wage inflation moderating and seems to be trending lower.

So, the Fed is raising rates to fight inflation; but it is possible that inflation outside of energy may already be rolling over.

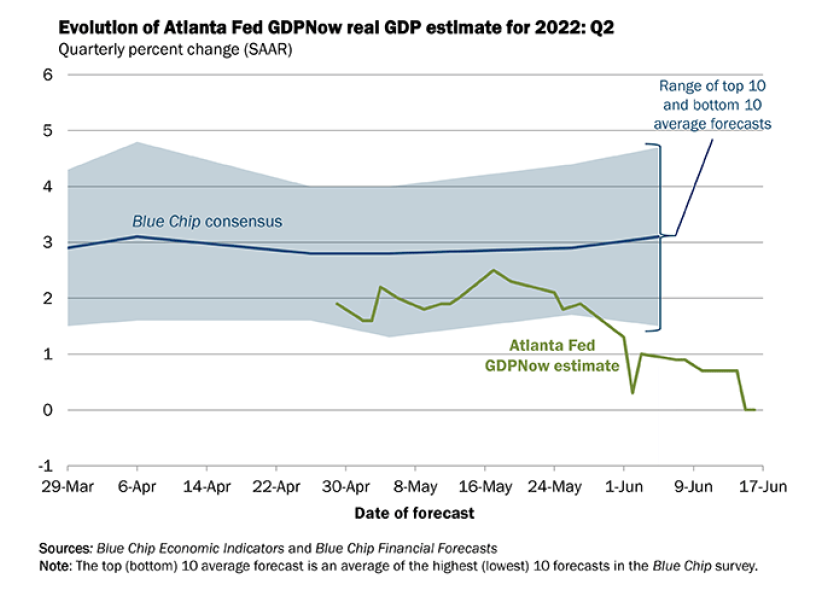

The consensus seems to be that recession is unlikely in the near term, with most economists projecting a potential recession sometime in 2023. However, we have already seen one negative GDP print and given the current backdrop it is entirely possible that we see another negative print at the end of the quarter. In other words, it would be naïve to dismiss the possibility that we are already in a technical recession (which would be the second in the last two years). In fact, the Atlanta Fed’s GDPNow model shows a significant divergence from the average forecast.

The Road Ahead:

Whether or not we are currently in a recession or on the precipice of one will likely come down to semantics and in any event, will not be clear until long after the fact. No matter what the Fed does with interest rates, they will not be able to effectively combat high energy prices unless they over-tighten, purposefully increase the unemployment rate and essentially throw us into an intentional recession. There is simply too wide a gap between current supply and demand driven by underinvestment in the energy complex and the supply disruptions created by the Russia / Ukraine conflict and China’s zero tolerance Covid policies.

Given the fact that markets are forward-looking in nature, it is reasonable to assume that most of the damage in risk assets has been done. The current drawdown in both equity and bond prices has been dramatic and based on historical bear markets may get worse before it gets better.

On the positive side, equity market returns tend to be above-average coming out of a technical bear market (defined as a 20% move down from the peak), averaging 22% to the upside in the first twelve months. Expect to see sharp rallies as the equity market tries to make a bottom that may turn out to be head fakes before a longer-term recovery trend ensues. The ascent of bond yields should also moderate as inflation expectations come down.

In our January 2022 Annual Outlook we highlighted the importance of that alternative strategies such as real estate, private credit and precious metals can play in an inflationary environment, particularly with increased correlations between stocks and bonds. We continue to believe this to be the case in the second half of the year.

Difficult markets are a necessary evil for investors, and the current environment is no exception. For many it can be difficult to stay the course in such times. We believe, and history has proven, that staying disciplined and unemotional during turbulent times is essential to long-term investing success.

As always, please reach out to us directly to discuss any of the above information further or with questions specific to your portfolio.

Sincerely,

Josh L. Galatzan, CIMA®

Founder & Managing Partner

Kirk Price

Managing Partner

Brian J. Noonan, CEPA

Managing Partner

Meagan Moll, CIMA®, CFP®, CPWA®

Partner & Wealth Advisor

The content of this publication should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors on the date of publication and are subject to change. Information presented should not be construed as personalized investment advice or as an offer to buy or sell, or a solicitation of any offer to buy or sell the securities mentioned. Content is derived from sources deemed to be reliable.

Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment or strategy will be suitable or profitable for an investor’s portfolio. All investments have the potential for profit or loss. Past performance does not ensure future investment success.

Index returns do not represent the performance of Meridian Wealth Advisors or any of its advisory clients. Historical performance results for investment indexes and/or categories, generally do not reflect the deduction of transaction and/or custodial charges or the deduction of an investment advisory fee, the incurrence of which would have the effect of decreasing historical performance results. There can be no assurances that an investor’s portfolio will match or outperform any particular benchmark.

Meridian Wealth Advisors, LLC is registered as an investment adviser with the SEC and only transacts business in states where it is properly registered or is excluded or exempted from registration requirements. SEC registration does not constitute an endorsement of the firm by the Commission nor does it indicate that the adviser has attained a particular level of skill or ability.