Q3 2021 Commentary: Not Quite as Bad as it Felt

Q3 2021 Commentary: Not Quite as Bad as it Felt

October 5th, 2021

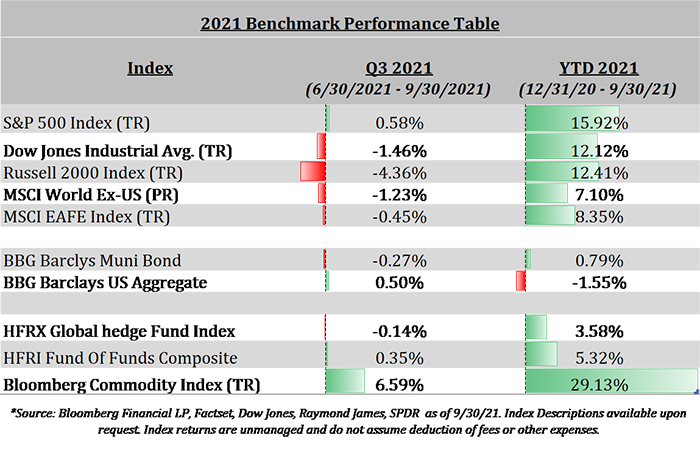

The third quarter wasn’t quite as bad as it may have felt to many investors. Worries surrounding pandemic risks, inflation pressures and government strife dominated the headlines and investor sentiment. While the quarter ended on a sour note with seasonally typical negative returns in most asset classes, the quarter overall saw mostly benign returns across the board. The exceptions were commodities to the upside (+6.59%), led by oil, and small caps (-4.36%) and emerging markets (-8.09%) to the downside.

The pandemics path and the reopening of the global economy remain at the center of the economic and investment backdrop. The surge in the Delta variant created a setback on this front but was firmly on the decline by the end of the quarter. However, persistent supply chain constraints have led to higher inflation that may very well be in the picture longer than the FOMC originally believed, which was particularly troublesome to investors in September as the 10 Year Treasury Yield spiked to 1.5%, oil raced to nearly $80 a barrel and equity market volatility increased dramatically. FOMC Chairman Powell also indicated that tighter monetary policy may be imminent via tapering (reduction in the pace of bond purchases being made by the Fed). And of course, Washington played its part as well. Republicans and Democrats remain miles apart on seemingly every issue save the negative impacts of social media on our society and specifically on our country’s children. The parties remain at loggerheads over President Biden’s proposed stimulus plan, immigration, pandemic response and most recently the raising of the debt ceiling. The potential for a US default on financial obligations in particular contributed to investor angst in September.

So where does that leave us heading into the fourth quarter? Is it all falling apart at the seams? While the talking heads on TV and the internet would have you believe so, we wouldn’t be too quick to turn decidedly negative. To be sure there are headwinds to face and concerns over the afore mentioned topics are legitimate. However, positive tailwinds remain in place, and we believe the economy will remain resilient for some time to come. Below we examine a few key issues that will likely drive investor behavior and market results for the remainder of the year.

The Debt Ceiling & Infrastructure

Let’s get this out of the way first. At the time of this writing Senator McConnell has proposed a short-term deal to lift the debt ceiling through December and avert a government shutdown and potential default on US obligations. By the time this is published, it will likely be agreed upon. While government shutdowns are not unusual (we have had 22 in the last 45 years) or typically impactful long term, the idea of a US default, even a technical default, is unprecedented. Were a default come to pass, the reputational risks alone would be irreversible. Interest rates would rise and financing costs for everyone from businesses and individuals to the government itself would increase. Equity markets would certainly react in a very negative way, and we would run the risk of derailing the economic recovery from the COVID-19 pandemic induced recession. Legislators are aware of this, and neither party wants to be viewed as responsible for such an outcome. We believe that they will come to terms on the debt ceiling both in the short and long term. The stakes are simply too high. Much of the strife over this issue has actually been political gamesmanship around the filibuster and infrastructure bill. A short-term deal kicks the can down the road and puts pressure on President Biden and congressional leadership to negotiate a smaller infrastructure deal or pursue the reconciliation process.

Inflation & the Fed

Prices have been rising all year due primarily to labor and supply chain constraints. Food, energy, computer chips…you name it. Policy makers are beginning to realize that inflation may be less transitory than they originally expected and the FOMC recently indicated that they may begin tapering the pace of bond purchases before the end of the year, thereby tightening monetary policy. The idea of higher rates and tighter monetary policy scares many investors. Slowing the pace of bond purchases does not mean that the Fed’s balance sheet will contract or that rates will necessarily rise. Overall monetary policy is and will remain very accommodative with the markets awash in liquidity. Importantly, we expect the Fed to keep rates at their current level into next year, which is supportive of the current recovery and risk assets.

COVID-19 & Reopening

The pandemic remains at the heart of everything these days, including the economic outlook. We learned the hard way the variants of the virus may prove more difficult to contain that the original. While the US and the world have made great strides in vaccinations, a significant percentage remain unvaccinated. However, re-opening presses forward and we view the risk of a return to widespread lockdowns as low. People in general are learning to live with the risk of the virus and the economy is responding. We expect economic growth to continue into next year, although at a slower pace than what we experienced early in the recovery.

Closing Thoughts

In general, we believe the economic recovery continues, supported by a strong consumer, accommodative monetary policy, and an improving employment backdrop. Corporate earnings have been strong and, in many cases, stronger than expected while balance sheets remain healthy at both a corporate and personal level. Higher and more persistent inflation, pandemic resurgence due to new variants and rich valuations in many asset classes remain clear risks and the political circus in Washington continues to influence nearly all of these issues. We remain generally constructive on the current environment with a bias towards equities, real estate and private equity over fixed income.

Looking ahead to 2022 we believe the outcome of President Biden’s infrastructure and tax plans will be of key importance to the path forward. We could dedicate pages to what has been proposed, but at this time it is rife with uncertainty and conjecture. Once we have definitive plans on both topics to analyze, we will communicate accordingly.

As always, please do not hesitate to reach out to us directly with any questions or to discuss further.

Sincerely,

Josh L. Galatzan, CIMA®

Founder & Managing Partner

Kirk Price

Managing Partner

Brian J. Noonan, CEPA

Managing Partner

Meagan Moll, CIMA®, CFP®, CPWA®

Partner & Wealth Advisor

The content of this publication should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors on the date of publication and are subject to change. Information presented should not be construed as personalized investment advice or as an offer to buy or sell, or a solicitation of any offer to buy or sell the securities mentioned. Content is derived from sources deemed to be reliable.

Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment or strategy will be suitable or profitable for an investor’s portfolio. All investments have the potential for profit or loss. Past performance does not ensure future investment success.

Index returns do not represent the performance of Meridian Wealth Advisors or any of its advisory clients. Historical performance results for investment indexes and/or categories, generally do not reflect the deduction of transaction and/or custodial charges or the deduction of an investment advisory fee, the incurrence of which would have the effect of decreasing historical performance results. There can be no assurances that an investor’s portfolio will match or outperform any particular benchmark.

Meridian Wealth Advisors, LLC is registered as an investment adviser with the SEC and only transacts business in states where it is properly registered or is excluded or exempted from registration requirements. SEC registration does not constitute an endorsement of the firm by the Commission nor does it indicate that the adviser has attained a particular level of skill or ability.