Global Turmoil

The start of the year has been marked by a steady stream of headline risks, ranging from concerns around private credit to fears that artificial intelligence could displace large segments of white-collar employment. Markets have been forced to digest new information almost daily, contributing to heightened volatility across asset classes.

Against this backdrop, one might expect the recent conflict involving Iran to have triggered a more pronounced reaction in financial markets—particularly as oil prices briefly surged above $100 per barrel. Yet the response from U.S. equities has been relatively muted.

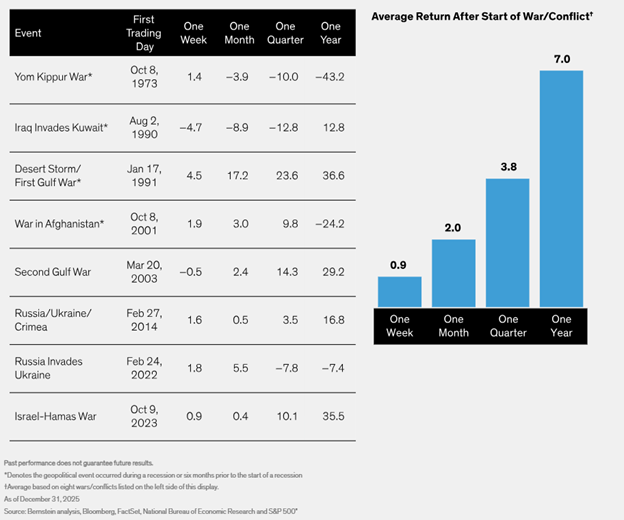

There are several possible explanations for this dynamic. First, the geographic distance between the United States and the conflict zone may be leading investors to view the situation with a degree of detachment—an “out of sight, out of mind” mentality. Second, some market participants may believe this conflict will resemble past regional flare-ups that ultimately prove short-lived and/or immaterial to markets in the long run, (e.g., recent Venezuela Operation Absolute Resolve, Russian Annex of Crimea, 1989 Invasion of Panama, Gulf War, Invasion of Grenada) - some of these shown in the market impact graphic below. Finally, investors may simply be taking a wait-and-see approach, choosing not to make significant portfolio adjustments until there is greater clarity around how the situation unfolds.

While these explanations carry merit, a deeper undercurrent may be driving market behavior. Over the past year, international equities have broadly outperformed U.S. markets. In times of geopolitical uncertainty, investors often rotate capital back toward U.S. assets, which are widely perceived as a relative safe haven. This reallocation could help explain why U.S. equities have remained resilient despite the escalation in the Middle East. Whether this trend proves durable remains uncertain, particularly if elevated oil prices begin to weigh on corporate margins.

Our current assessment is that markets may be underestimating the potential for this conflict to persist longer than the “few weeks” timeline suggested by policymakers. While the United States maintains one of the most sophisticated and capable militaries in the world, Iran possesses several strategic moves that could prolong the conflict. These include the use of relatively inexpensive drone technology and a decentralized command structure that makes it more difficult to disable leadership and operational capacity through targeted strikes.

Iran is also well aware that sustained pressure on energy markets can create economic and political pressure abroad. Roughly one-fifth of the world’s oil supply passes through the Strait of Hormuz, making it one of the most strategically important energy chokepoints in the global economy. Disruptions to shipping routes or attacks on regional energy infrastructure could therefore place upward pressure on oil prices and feed through to broader inflation via higher transportation, manufacturing, and input costs.

Oil and gas equities have already experienced a strong rally in recent months and could continue to benefit if energy prices remain elevated. However, the magnitude of that upside may be tempered by industry hedging practices. Many producers hedge a significant portion of their future production well in advance, often with price ceilings in the mid-to-high $60 range, which can limit near-term gains from rising spot prices.

Ultimately, history has proven that performance has typically stayed intact within the year of a conflict taking place despite short-term volatility. However, this situation does reinforce a broader theme that has emerged since the COVID-19 pandemic: the strategic importance of resilient supply chains and domestic production capacity. For many governments and corporations alike, national security and economic security are becoming increasingly intertwined.

As always, please do not hesitate to reach out directly to our team for further discussion.

Regards,

|

Josh L. Galatzan, CIMA® |

Kirk Price |

|

Chris J. Popso |

Brian J. Noonan, CEPA |

|

Meagan Moll, CIMA®, CFP®, CPWA® |

The content of this publication should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors on the date of publication and are subject to change. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such. Information presented should not be construed as personalized investment advice or as an offer to buy or sell, or a solicitation of any offer to buy or sell the securities mentioned. Content is derived from sources deemed to be reliable. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur.

Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment or strategy will be suitable or profitable for an investor’s portfolio. All investments have the potential for profit or loss. Past performance does not ensure future investment success.

Index returns do not represent the performance of Meridian Wealth Advisors or any of its advisory clients. Historical performance results for investment indexes and/or categories, generally do not reflect the deduction of transaction and/or custodial charges or the deduction of an investment advisory fee, the incurrence of which would have the effect of decreasing historical performance results. There can be no assurances that an investor’s portfolio will match or outperform any particular benchmark.